UPI, or Unified Payments Interface, is a real-time, instant payment system handling over 85% of all digital transaction volume in India as of late 2025. As a dominant method, over 80% of the users who perform online banking transactions prefer to use only UPI. As a result UPI handles roughly 20 billion transactions monthly, that is 7,500 transactions per second. This is huge and it is developed and maintained by NPCI.

Why do we need UPI?

Before UPI and now also there are digital banking methods like NEFT, IMPS and RTGS for electronic transitions exist,

NEFT (National Electronic Funds Transfer): It allows individuals and corporates to transfer funds between bank branches on a batch-processed basis. Also here the transactions are settled in half-hourly batches.

IMPS (Immediate Payment Service): Transfers happen in real-time, even on holidays, 24 hours a day, 365 days a year. Enables money to be sent to accounts in different banks across India. But this method requires knowing the recipient's account, IFSC and bank.

RTGS (Real Time Gross Settlement): It is secure electronic system for large-value fund transfers, where payments are settled individually and instantly through central bank's books. This method reserved mostly for business/payment above a threshold.

All these systems have some or the other drawbacks like takes long time for the transaction to happen, need of knowing recipient's account, IFSC and bank. Imagine for a ₹10 payment you need to ask the recipient for his account details and wait for hours for transaction to happen. It's not feasible right, we need a system which is fast, real-time, instant transactions supported and we don't have to know the recipient's bank details. And UPI is that system.

What is Unified Payments Interface (UPI) :

As of know we understood why we need UPI. Now we will know more about UPI. Unified Payments Interface is a real-time, instant payment system developed by National Payments Corporation of India (NPCI), launched in August 2016.

This system facilitates money transfers between bank accounts via smartphones. UPI operates 24/7, 365 days a year. UPI works by leveraging existing systems, such as Immediate Payment Services (IMPS) and Aadhaar Enabled Payment System (AEPS), to ensure seamless payment settlement between bank accounts. And it eliminates the need of to know recipient's bank details for each payments, simplifying payments through QR codes, virtual payment addresses (VPAs), or UPI-registered mobile numbers.

Features of Unified Payments Interface (UPI) :

Instant Transactions : UPI works 24/7, 365 days a year. Whether it’s 2 AM on a Sunday or a public holiday, the money moves instantly from your account to theirs.

Unique Identifier : UPI eliminates the need of knowing recipient's bank account details. With UPI, your bank account gets a "handle" like yourname@bank. It's like a social media username, but for your money. It keeps actual bank details private and secure.

Multiple Account Linking : You don't need an app for every bank account you own. You can link your any number of bank accounts into one UPI app (like GPay, PhonePe, or BHIM). It's a single dashboard for entire financial life.

Secure Transactions : UPI uses "Two-Factor Authentication". To pay money you need to have your phone (which has your SIM) and you need to enter your secret MPIN. Even if someone knows your password, they can't do anything without your specific device.

Collect Requests : This is a feature where receiver requests money, and the payer approves the payment. This feature is mainly used in shops to request an exact payment amount from customers, ensuring accuracy, security and explicit user consent before money is transferred.

QR Code Payment : This is the heart of Indian street market. From mall to a roadside tea stall, just scan the code and pay. It's contactless, fast and you don't have to worry about change.

UPI Autopay : It is a feature that allows users to set up recurring payments for subscriptions or bills, where money is automatically debited at fixed intervals after one-time authorization.

UPI Lite X : If you're in a place with no signal, you can still pay using UPI Lite X.

UPI Circle : Want to let your younger sibling buy stationary's but don't want to give them their own bank account? UPI circle lets you "delegate" payments. You set a limit, and they can pay using your account, but you stay in control of the permissions.

UPI is Going Global : You don't always need a Forex card anymore. From Singapore to France and the UAE, more countries are starting to accept UPI. You can pay in Indian Rupees, and the system handles the conversion behind the scenes.

Key Participants in UPI :

NPCI (National Payments Corporation of India) : Operates the central switch, manages the UPI infrastructure, ensures interoperability and sets protocols.

Issuer Bank : The user's bank that initiates the transaction and debits the account.

Beneficiary Bank : The receiver's bank that receives and credits the funds.

Payment Service Providers (PSPs) : Apps like PhonePe, GPay, Paytm, etc. These are PSPs which provide the interface to connect to UPI network through partner banks.

Users and Merchants : Bank account holders who initiate/receive payments and businesses accepting UPI payments.

Functional and Non-Functional Requirements :

Functional Requirements :

User Registration and Authentication : This includes linking of mobile number to bank accounts and creation of a unique Virtual Payment Address (VPA).

Secure Transactions : 24/7 instant fund transfers using UPI PIN for transaction authorization and support for biometric authentication.

Fund Transfer Mechanisms :

Push (Pay) : Initiating a payment to another user/merchant.

Pull (Collect) : Requesting payment from another user.

QR Code Payments : Generating and scanning QR codes for quick, contactless payments.

Bank Account Management : Linking and managing multiple bank accounts in a single app.

Transaction History : Access to detailed records, including timestamps and transaction status.

Real-time Notification : There should be instant alerts for successful or failed transaction, also for the otp verification.

Bill Payments : Support payment of bills like electricity, fastag, etc. Through the UPI interface.

Non-Functional Requirements :

Scalability : The system should handle millions of transactions per day (600+ million transactions daily).

Performance : Ensure low latency for real-time transaction processing and instant processing status providing.

Reliability : Ensure high availability with minimal downtime. Implement failover mechanisms to handle system failures gracefully.

Consistency : ACID guarantees to prevent double-spending and discrepancies.

Security : Implementation of security measures to protect user data and financial transactions. Multi-layered encryption on the user payment details.

Usability : Design a user-friendly interface that is easy to navigate. Ensure accessibility for users with different levels of technical expertise.

Capacity Estimation :

Traffic Estimate :

Total Registered Users: ~450 million (Unique users across apps like PhonePe, GPay, Paytm).

Daily Active Users (DAU): ~150 million users.

Transactions per User per Day: 4.5 transactions (Weighted average across high-frequency P2M and P2P).

Total Daily Transactions: ~650 million transactions.

Peak Load (TPS): ~30,000 Transactions Per Second (to handle morning/evening surges).

Storage Estimation :

Average Transaction Size: 1 KB.

Daily Data: 650 million × 1 KB = ~650 GB/day.

Monthly Data: 650 GB × 30 = ~19.5 TB/month.

Yearly Data: 19.5 TB × 12 = ~234 TB/year.

Note: This accounts for the primary transaction ledger. Backup and audit logs typically triple this requirement.

Bandwidth Estimation :

Request/Response Size: 2 KB (Combined total per transaction round-trip).

Total Daily Requests: 650 million.

Total Daily Data Transfer: 650 million × 2 KB = ~1.3 TB/day.

Average Bandwidth Speed Required: ~125 Mbps (sustained), with peak bursts requiring 1.5 Gbps+ capacity.

Memory Estimation :

Active Users to Cache (Peak): 25 million (Concurrent sessions/frequent transactors).

Data per User: 4 KB (Includes VPA info, linked bank metadata, and risk-score fragments).

Total Memory (RAM): 25 million × 4 KB = ~100 GB.

UPI Transaction Flow :

The UPI Transaction flow outlines the steps involved in processing payments. There are two main flows they are, Payment initiated by the sender (push) and Payment requested by the recipient (pull).

Payments Initiated by the Sender (Push) :

This allows user to initiate payments directly from there accounts to transfer money to a recipient. This method is commonly used for purchases, bill payments or sending money to friends and family.

Phase 1 : Transaction Initiation and Authorization

Payer initiates the payment using any UPI-enabled apps to scan the QR-code or enter recipients details and the transaction amount.

The app then forwards the transaction request to their chosen Payment Service Provider (PSP), which acts as an intermediary.

Then PSP routes the request to the NPCI server, which validates both payer and receiver's VPA.

The issuing bank verifies the transaction's authenticity, checks account balance, and confirms customer credentials.

After verification the issuing bank authorizes the transaction and generates a digital signature for security.

Phase 2 : Verification and Money Transfer

The PSP shares the sender's bank details with the UPI system.

The NPCI servers checks account details and balance availability. If sufficient amount is present then server triggers deduction from the sender's account.

The receiver's bank receives the transaction amount and credits it to the payee's account.

The UPI server sends a response to the customer's app, along with a reference ID.

Payment Request from Receiver's (Pull) :

Pull system allows recipients to initiate a request for transfer from sender. This method is often used for bill payments or collecting payments from customers.

Phase 1 : Initiation of transaction and Payment Message sending

The recipient generates a payment request using UPI enabled app.

The request is sent to NPCI server.

Phase 2 : Transaction Flow between Banks

The payment first goes to creditor's bank, then the bank forward the request to debtor's bank through NPCI.

The debtor's bank verifies the request and check the availability of balance.

If the balance is available then the debtor's bank confirms the transaction to NPCI.

The debtor's bank transfers the requested amount to the creditor's bank.

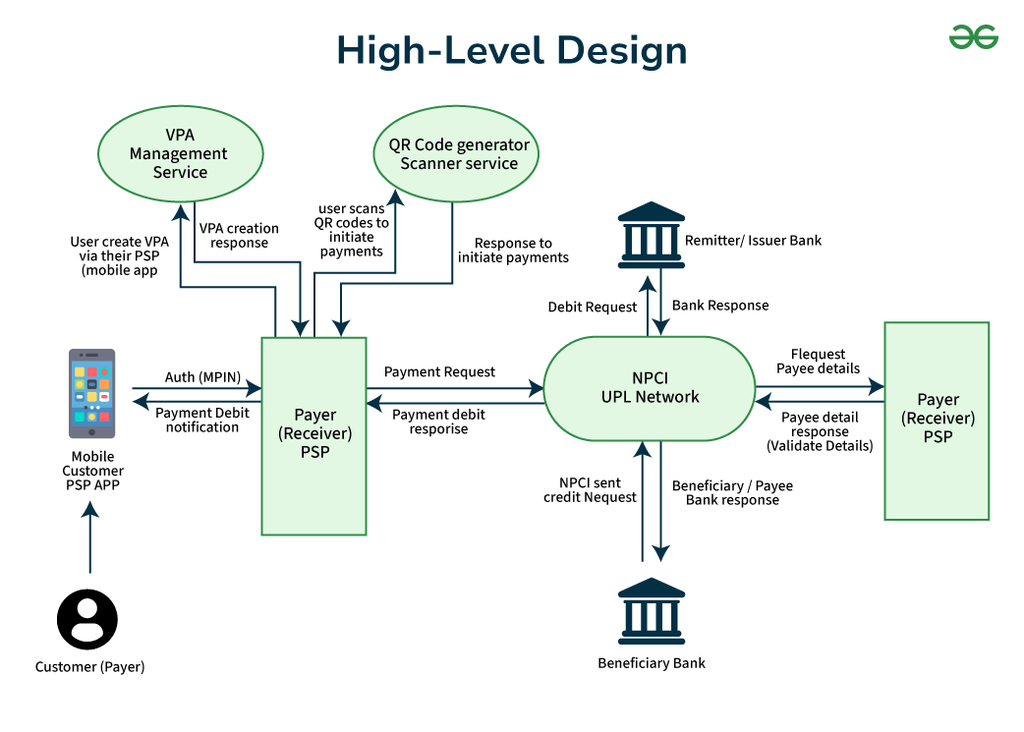

System Architecture :

Image Credits : Geeks for Geeks

Low Level Architecture Components:

The UPI Switch (NPCI): A central, "stateless" router. It doesn't store your money; it just directs traffic between banks using O(1) lookup speeds.

PSP Adapters: Small software layers that translate the bank's old internal language into modern UPI language.

HSM (Hardware Security Module): A dedicated "safe" inside the bank that handles your PIN encryption. Even bank employees can't see your PIN.

Kafka Event Bus: A high-speed "conveyor belt" that carries transaction logs and notifications to different services without slowing down the main payment.

Zonal Replication: Data is mirrored across multiple "Availability Zones." If one data center in Mumbai fails, the Bengaluru center takes over instantly.

Is UPI Actually Safe?

UPI isn't just convenient; it’s built on a "Zero-Trust" security framework mandated by the RBI. Here’s how it protects you:

Bank-Grade Encryption: Every transaction is shielded by AES (Advanced Encryption Standard) and TLS 1.3 protocols, ensuring your data is unreadable to hackers during transit.

Virtual Identity (VPA): By using a UPI ID (like name@bank), you never have to share your actual bank account number or IFSC code with merchants.

Device Binding (Hardware Lock): Your account is cryptographically tied to your specific mobile device and SIM card. Even if someone knows your PIN, they cannot transact from another phone.

Mandatory 2FA: Every payment requires Two-Factor Authentication—usually something you have (your phone) and something you know (your 4-6 digit MPIN).

Risk Mitigation Limits: Default daily transaction limits (usually ₹1 Lakh) and per-transaction caps act as a "circuit breaker" to minimize potential loss from fraud.

RBI-Backed Protection: Strict regulatory oversight means every transaction is backed by a formal dispute resolution framework, allowing you to flag unauthorized charges instantly.

Problems UPI solves :

Before 2016, moving money was a chore. UPI didn't just add a new feature; it fixed a broken system.

The "Chutta" (Small Change) Problem: No more hunting for ₹5 or ₹10 notes at the grocery store. UPI made micro-payments so easy that even street vendors stopped asking for exact change.

The Banking Hours Barrier: Traditional systems like NEFT worked in "batches" and slept on weekends. UPI introduced 24/7/365 instant settlement. If it’s 3 AM on a Diwali night, the money still moves.

The "Account Detail" Nightmare: You used to need a Name, Account Number, and a 11-digit IFSC code just to send ₹100. UPI replaced that mess with a simple VPA (Virtual Payment Address)—like an email ID for your money.

The "Too Many Apps" Fatigue: Instead of having one app for HDFC, one for SBI, and another for ICICI, UPI gave us Interoperability. You can use any app (GPay, PhonePe, BHIM) to access any bank account you own.

High Transaction Costs: Credit and Debit cards often come with MDR (Merchant Discount Rate) fees that eat into a small shopkeeper's profit. UPI’s Zero-MDR model made digital payments free for most merchants.

The "Is it Success or Failure?" Guesswork: Before UPI, if a digital payment failed, you’d wait days to know why. UPI provides Real-Time Confirmation for both the sender and the receiver instantly.

Cash-on-Delivery Hassles: UPI became the perfect "digital cash" for e-commerce. No more running to the ATM because the delivery partner doesn't have a card machine.

How is UPI Different from IMPS ?

Feature | IMPS (Immediate Payment Service) | UPI (Unified Payments Interface) |

The Foundation | The original "Real-Time" rail launched in 2010. | An advanced layer built on top of IMPS (2016). |

Address | Needs Account No. + IFSC or MMID. | Needs a simple UPI ID (VPA) or QR Scan. |

Transaction Flow | Push only: You can only send money. | Push & Pull: You can send and request money. |

App Experience | Tied to your specific Bank’s app. | Interoperable: One app for all your banks. |

Cost | Usually costs ₹2 to ₹25 + GST. | Free for personal peer-to-peer use. |

Limits | High value (often up to ₹5 Lakh). | Daily limit (usually ₹1 Lakh). |

Mechanisms The Helps in Scalability of UPI System :

The Architecture :

Microservices: The system is split into small, independent parts. If one fails, the others keep working.

Adding Servers: Instead of one big server, the system adds hundreds of small ones to handle peak traffic.

Always Online: Data is copied across multiple locations. If one center goes down, the system stays up.

Fast Databases: It uses modern databases like Cassandra to handle millions of users at the same time.

The Engine :

Smart Queues: Tasks like "sending a message" happen in the background so your payment clears faster.

Memory Caching: It uses Redis to store common data in "fast memory" instead of a slow disk.

One-Time Charge: The system is "Idempotent." Even if you hit "Pay" twice by mistake, you only get charged once.

The Network :

Private Highway: Banks talk to each other over a private, high-speed line (MPLS) for extra security.

Lightweight APIs: The code is designed to be "small" so it travels across the internet instantly.

Smart Load Balancers: Your request stays with the same server from start to finish to save time.

Specialized Solutions :

UPI Lite X: Handles small payments offline using NFC (Tap to Pay) to save the bank's server load.

Smart Routing: If one bank’s server is slow, the system automatically finds a faster path.

Blockchain Autopay: Recurring bills (like Netflix) are now tracked on a secure, permanent digital ledger.

How Errors and Failures are Handled?

The Saga Pattern: UPI uses a "Saga" model. If a payment fails halfway (money debited but not credited), the system automatically triggers a Reversal to put the money back.

Eventual Consistency: The system doesn't wait for everything to be perfect. If a bank server is slow, the transaction is marked "Pending," and a background process finishes it later.

Automatic Retries: For small network glitches, the system retries the request behind the scenes before telling you it failed.

Idempotency Keys: Every request has a unique ID. If you hit "Pay" twice due to a laggy screen, the system sees the ID and ignores the second request to prevent double-charging.

Timeout Management: If a bank doesn't respond within a few seconds, NPCI cuts the connection and starts the refund process immediately.

Significant Changes in UPI 2.0 :

Overdraft Facility : Users can link their overdraft accounts to UPI.

One-Time Mandate : Enables pre-authorizing transactions, where funds are blocked and debited on a future date (useful for subscriptions or e-commerce).

Invoice in the Inbox : Merchants can send an invoice, allowing users to verify transaction details before paying.

Higher Transaction Limits: Facilitates larger transactions beyond the standard ₹1 lakh limit.

Linking Multiple Accounts : Users can link multiple bank accounts to a single UPI handle.

Signed Intent and QR : Enhanced security that verifies merchant authenticity, protecting against fraud.

Working with UPI Systems :

If you’re a developer shipping a product today, you don't need to build a bank. You just need a good API. Most gateways (like Razorpay or Cashfree) make it look like this:

Smart Multi-Bank Routing: The system automatically picks the fastest bank server so your customers don't see a "Transaction Failed" screen.

Developer-Friendly APIs: Simple REST APIs and SDKs that let you add a "Pay Now" button in just a few lines of code.

Instant Refunds: No more manual entries. If a payment needs to go back, the API handles the reversal in one click.

Real-Time Webhooks: Your server gets an instant "ping" the moment a payment is successful.

UPI AutoPay: Great for SaaS or subscriptions. You set the logic once, and the money is collected automatically every month.

Unified Dashboard: See your success rates, failures, and settlements all in one clean UI.

New Features and Updates :

Credit Line on UPI (CLOU): You can now pay using credit directly through UPI. It’s basically a virtual credit card without the plastic.

Project Nexus (Global UPI): You can now pay at shops in Singapore, UAE, and France using the same QR code you use at home.

AI Fraud Shield: Gateways now use real-time AI to block "suspicious" payments before they even happen, keeping your business safe from scams.

Conclusion:

UPI has officially moved from a "cool feature" to the backbone of the Indian economy. For us developers, it's a dream because it's built on open standards and clean APIs.

If you aren't integrating UPI into your app in 2026, you're building in the past. It’s fast, it’s free (mostly), and it’s the most advanced payment tech in the world right now.